November 8, 2022 will obviously be remembered in history as the day of the U.S. mid-term elections, but could another event that happened yesterday eclipse even the national elections?

Earlier this year I warned that cryptocurrencies were NOT safe havens to protect financial wealth, when Coinbase, the largest US crypto exchange service, announced that they had cut off 25,000 Russian wallets.

As I noted then, I have never felt comfortable putting major resources into cryptocurrencies for several reasons, the most obvious one being that it is dependent upon “the system,” which requires, among other things, electricity and a working Internet.

New problems with cryptocurrencies were exposed yesterday, when the equivalent of a “bank run” happened when crypto exchange FTX saw $6 billion of withdrawals in a 72-hour span, resulting in them reportedly stopping the process of withdrawals yesterday.

Some big investors, including Blackrock and celebrity athletes including Stephen Curry and Tom Brady, were heavily invested in FTX.

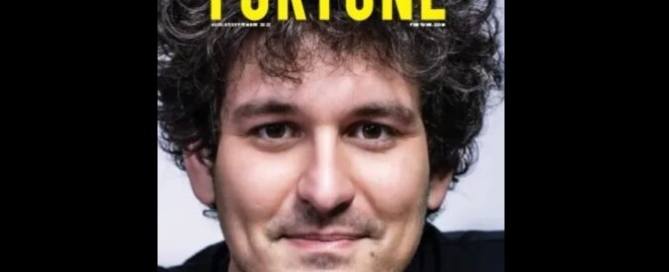

Sam Bankman-Fried, once featured on the cover of Fortune Magazine as potentially the next “Warren Buffet,” and has now reportedly lost 94% of his $16 billion fortune, may be better compared to Bernie Madoff, as ZeroHedge News found an interview he did a few months ago where he admitted that crypto yield farming is basically a Ponzi business.

The big question now is when will the other big Ponzi scheme rupture, the New York Stock Exchange, sending the U.S. and probably the rest of the world into financial ruins and usher in the Great Reset?