by Brian Shilhavy

Editor, Health Impact News

It’s been over a week now since a bank has failed, but according to multiple sources, that does not mean that the banking crisis is over.

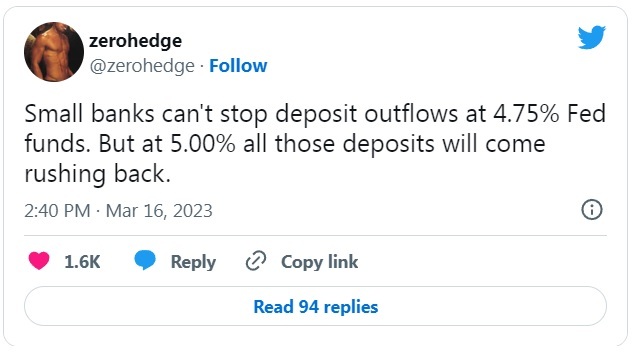

In fact, many sources are reporting that bank runs are continuing, with a “second wave” of bank runs now going on.

“Depositors Have Finally Awoken”: The Second Wave Of The Bank Run Has Begun, Barclays Warns

It may seem like an eternity ago, now that we stuff a month’s worth of trading and newsflow in a day, but it was exactly one week ago that Bill Ackman – who may or may not be long regional banks and/or commercial real estate – took to Twitter to bash Janet Yellen for restarting the bank run that defined much of the middle of March, when she unexpectedly told Congress that the Treasury was not considering a broad increase in deposit insurance, a line which promptly sent stocks tumbling.

Barclays’ in-house repo guru Joseph Abate – the bank’s equivalent to CS’ Zoltan Pozsar and BofA’s Mark Cabana – is out with a note, warning that while the first, acute wave of deposit outflows may be over now that the government has scrambled in its attempt to contain the fallout that is primarily the result of the Fed’s aggressive rate hikes…

… a second, slower-burning but even more powerful, bank run wave has now begun.

In the note, Abate – who says that “bank deposits are in the midst of a two-stage shift” – explains the In the first phase of the bank run, deposits were pulled from banks driven by “solvency concerns.” But as solvency fears fade, a second stage is emerging, one driven by interest rate differentials primarily between regional banks – who as we have noted before are unable to match the Fed Funds rate…

… and money market funds, which offer not only higher rates but a far safer asset base as collateral,to wit:

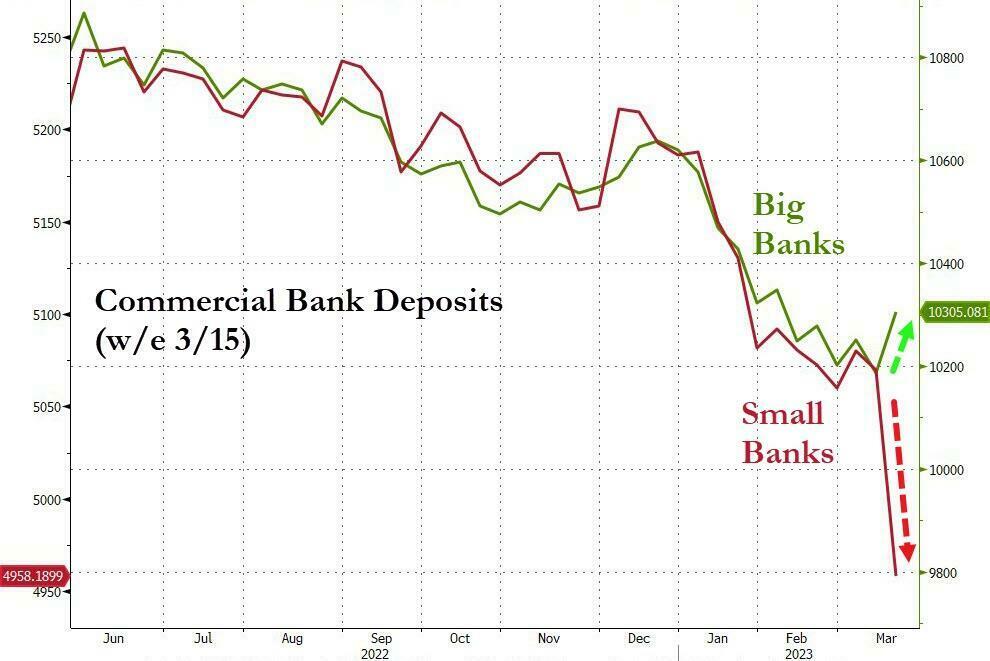

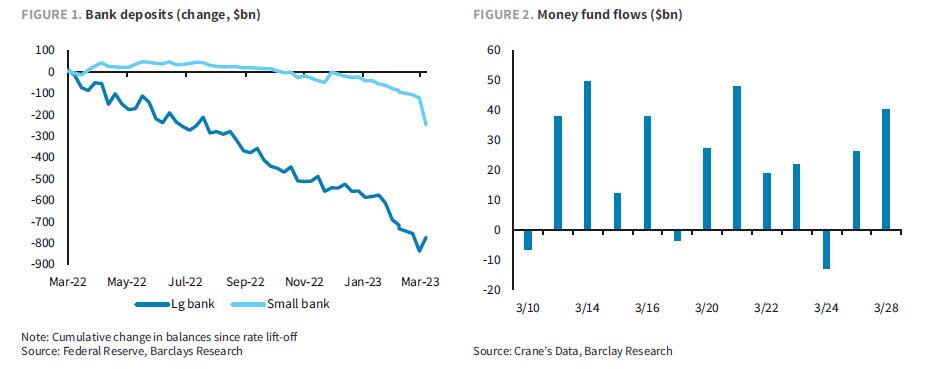

We suspect that banks are in the midst of a two-stage shift in deposit balances. Bank solvency concerns triggered the first wave of outflows. During this wave, balances have shifted from small to large institutions. Between March 1 and 15, deposits at the largest 25 banks fell about $20bn, but the decline in balances at small banks has been much steeper. Their deposit loss over the period ($140bn) is particularly acute, as these banks have been able to retain deposits more successfully than their larger competitors since lift-off (Figure 1).

At the same time, money fund balances have risen about $135bn. Inflows have since continued, with overall balances rising an additional $200bn – mostly into gov-only money funds (Figure 2).

(Full article.)

The first wave of deposit outflows is nearly over. A second wave has already started

The federal government’s efforts to backstop the banking system, and deals found to put SVB Financial and Signature Bank in new ownership, seems to have stabilized the financial sector, and calmed markets.

Joseph Abate, an interest-rate strategist at Barclays, says the Federal Reserve’s establishment of the Bank Term Funding Program as well as the abundant cash raised from advances borrowed from Federal Home Loan Banks has allowed banks to accumulate large buffers to meet deposit outflows. “And while market psychology is still fragile, our sense is that deposit outflows from small to large banks will fade as depositors recognize they can access and transfer their balances without any hitches,” says Abate.

But Abate says a second wave of deposit departures has started — to money-market funds. Depositors generally have kept their money in banks despite paltry returns, usually thanks to the broad array of services that banks provide, as well as what Abate calls “deposit rate inattentiveness.”

“It is too hard to shift balances or to establish a new relationship with another institution unless there is a large, convincing yield pickup. But some of it could reflect the fact that after 15 years of near-zero rates, depositors are not in the habit of paying much attention to the yield on their cash balances,” he says.

Whatever the reason, depositors now see they can earn more yield in a money market fund with potentially less risk, Abate says. (Source.)

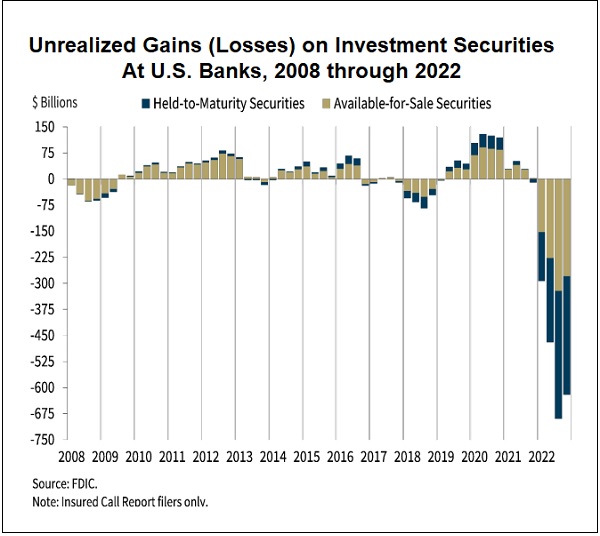

As Senate Banking Committee Convenes Hearing on Exploding Banks, an FDIC Chart Shows the Banking Crisis Is Far from Over

The two banks that failed and were taken over by the Federal Deposit Insurance Corporation (FDIC) were Silicon Valley Bank (SVB) and Signature Bank. Both had experienced bank runs in March and both had extreme exposure to uninsured deposits. One of the witnesses at today’s hearing, Martin Gruenberg, Chair of the Federal Deposit Insurance Corporation (FDIC), explains as follows in his written testimony for today’s hearing:

“A common thread between the failure of SVB and the failure of Signature Bank was the banks’ heavy reliance on uninsured deposits. As of December 31, 2022, Signature Bank reported that approximately 90 percent of its deposits were uninsured, and SVB reported that 88 percent of its deposits were uninsured. The significant proportion of uninsured deposit balances exacerbated deposit run vulnerabilities and made both banks susceptible to contagion effects from the quickly evolving financial developments. One clear takeaway from recent events is that heavy reliance on uninsured deposits creates liquidity risks that are extremely difficult to manage, particularly in today’s environment where money can flow out of institutions with incredible speed in response to news amplified through social media channels.”

Gruenberg has included a chart in his written testimony that is nothing short of stunning. (See chart above.) It shows that the unrealized losses on investment securities at federally-insured U.S. banks during the 2008 financial crisis were less than $75 billion while at the end of the fourth quarter of 2022 they were over $600 billion.

Also, the chart above does not capture the losses and contagion the Wall Street banks themselves created in the broader financial system through their bundling and selling of hundreds of billions of dollars of toxic subprime mortgage debt and derivatives.

Full article here. See also:

The Banking Crisis Knock-On Effect Has Been a Stampede into Government Money Market Funds – Foiling the Fed’s Effort to Raise Market Interest Rates

On Sunday, Financial Times reporters Brooke Masters, Harriet Clarfelt and Kate Duguid published an article under the headline: “Money market funds swell by more than $286bn as investors pull deposits from banks.” (Full article.)

As we have previously reported, these modern-day bank runs are not always as noticeable today in the digital era, as you don’t typically see people lining up at the banks to physically withdraw their money, as it all happens on the Internet.

And while today depositors are rushing into Money Market accounts, once the smaller banks start failing again, expect to see more money exit bank accounts, such as into the FedNow CBDC accounts scheduled to come online this summer, as well as into commodities such as Gold and Silver.

Are We Approaching The End Of The Dollar Reserve Currency System?

The rest of the world is, of course, noticing this, and some are beginning to trade with currencies other than the U.S. Dollar.

France Buys 65,000 Tons Of LNG From China In First Ever Yuan-Denominated Trade

China has just completed its first trade of liquefied natural gas (LNG) settled in yuan, the Shanghai Petroleum and Natural Gas Exchange said on Tuesday. As OilPrice notes, the Chinese state oil and gas giant CNOOC and TotalEnergies completed the first LNG trade on the exchange with settlement in the Chinese currency, the exchange said in a statement carried by Reuters.

The trade involved around 65,000 tons of LNG imported from the United Arab Emirates (because China will never admit that it is re-exporting Russian LNG even though it now does it all the time) the Shanghai Petroleum and Natural Gas Exchange added.

The French supermajor, one of the world’s top LNG traders, confirmed to Reuters that the trade involved LNG imported from the UAE, but declined to comment further on the deal.

France bought 65,000 tons of LNG using the Chinese yuan

The liquified natural gas was bought from the UAE, the payment is settled in the Shanghai Petroleum and Natural Gas Exchange, using Chinese yuan

We are witnessing the end of the US dollar hegemony. pic.twitter.com/GfX17nKxA1

— Zhao DaShuai 无条件爱国🇨🇳 (@zhao_dashuai) March 29, 2023

Read the full article here.

Goldman: “Are We Approaching The End Of The Dollar Reserve Currency System”

Last week was book-ended with a focus on CS/UBS on Monday and a focus on Deutsche bank on Friday. FOMC came and went with a consensus read of a 25bps dovish hike that came alongside some reassurance that the end of the tightening cycle is near (language shift from ‘ongoing’ hikes to ‘additional policy firming may be appropriate’). That being said, the US regional banking pressures persist… albeit with no ‘new’ bad news to deal with and First Citizens trading up over 50% on the back of SVB acquisition news…The European banks recovering from a bout of extreme and aggressive de-grossing.

In 2008 there was a credit issue coupled with a leverage issues. The Banks were the large and flexible balance sheets but could not offset the scale of the credit impairment or the scale of the leverage.

Today we have seen a shift of balance sheets from traditional and regulated spaces (banks) to less visible (private credit)… large… but inflexible balance sheets.

I think we are in the midst of dramatic regime change.

Is this 08? Or is it 1929? Is it a liquidity issue or a solvency issue? Is this a financial system issue?

There have been many arguments put forward about what ‘this’ is or ‘where’ we are.

One I have heard is that we are approaching the end of a $ reserve currency system and moving towards a more multipolar reserve system. (Full article. Subscription needed.)

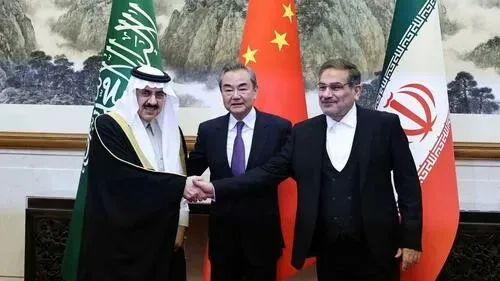

Saudi Arabia to Join Shanghai Cooperation Organization

On Wednesday, Saudi Arabia’s cabinet approved a decision for Riyadh to join the Shanghai Cooperation Organization (SCO), a Eurasian security and economic bloc that was founded in 2001 by China, Russia, and several Central Asian countries.

According to Saudi state media, Riyadh has approved a memorandum that would make Saudi Arabia a dialogue partner of the SCO, the first step toward a permanent membership.

The news comes as Saudi Arabia is moving closer to Beijing, raising concern in Washington. According to Reuters, Riyadh joining the SCO was discussed when Chinese President Xi Jinping visited Saudi Arabia in December.

Saudi Arabia and China have agreed to increase cooperation in all areas during Xi’s visit. The Wall Street Journal reported this month that Riyadh is in talks with Beijing on pricing its oil in the yuan, a move that could impact the US dollar’s dominance.

Saudi Arabia’s decision to join the SCO comes after China brokered a surprise normalization deal between Riyadh and Tehran. Last year, Iran signed a memorandum to become a permanent member of the SCO, which is expected to become official this year. Other permanent members include India, Pakistan, Kazakhstan, Kyrgyzstan, Tajikistan, and Uzbekistan.

The SCO is a significant economic bloc as its members make up half of the entire world’s population. Iran’s ascension into the SCO will help the country weather US and other economic sanctions as it will help increase trade with Russia, China, and other major economies. (Full article.)

De-Dollarization Just Got Real

by John Rubino

Excerpts:

Since the 1970s it’s been virtually impossible for a country to function without access to US dollars. And Washington maintained this highly-favorable status quo by putting various kinds of pressure — from sanctions to election theft to outright invasion — on anyone who stepped out of line.

This weaponization of the world’s reserve currency has, not surprisingly, created resentment in a lot of foreign capitals. And after a long gestation period, that resentment is now erupting into a rebellion against dollar hegemony. Among the big recent events:

The BRICS coalition has become the hottest ticket in geopolitics. Brazil, Russia, India, China, and South Africa (the BRICS) have been toying with the idea of forming a political/monetary counterweight to U.S. dominance since 2001. But beyond some aggressive gold buying by Russia and China, there was more talk than action.

Then the floodgates opened. Whether due to the pandemic’s supply chain disruptions, heavy-handed sanctions imposed by US-led NATO during the Russia-Ukraine war, or just the fact that de-dollarization was an idea whose time had finally come, the BRICS alliance has suddenly become the hottest ticket in town. In just the past year, Argentina, Indonesia, Saudi Arabia, Iran, Mexico, Turkey, the United Arab Emirates (UAE), and Egypt have either applied to join or expressed an interest in doing so. And new bilateral trade deals that bypass the dollar are being discussed all over the place.

Combine the land mass, population, and natural resources of the BRICS countries with those of the potential new members and the result is more or less half the world. And now things are getting real:

China brokers a peace deal between Saudia Arabie and Iran, two bitter historical enemies who want to join the BRICS alliance but can’t if they’re in an undeclared war. Should they stop competing and start cooperating they could dominate the Middle East and raise China’s clout in the region, at the petrodollar’s expense. An example of the press coverage:

Eurasia’s geo-economic integration took a great leap forward as a result of the Iranian–Saudi rapprochement, which unlocks the Gulf Cooperation Council’s (GCC) trade potential with Russia and China. Its wealthy members can now tap into two series of Iranian-transiting megaprojects in one fell swoop through this deal, with the North-South Transport Corridor (NSTC) connecting them to Russia while the China-Central Asia-West Asia Economic Corridor (CCAWAEC) will do the same vis-à-vis China…

…Only two weeks after Saudi Arabia announced an effort to establish diplomatic ties to Iran in a deal mediated by China, more news surfaced that Saudi Arabia was also planning to reopen its embassy in Syria for the first time in over a decade. Rumors are swirling that Iran, Saudi Arabia and Syria are on the verge of geopolitical and economic agreements that sidestep the US.

Russia and India agree to trade oil for rupees. Russia is now India’s largest oil supplier, with 35% of that massive, growing country’s imports. The U.S. is not happy about this — but India doesn’t seem to care. From a recent article:

Even the US itself seems to have finally accepted that it can’t reverse this trend, which is evidenced by former Indian Ambassador to Russia Kanwal Sibal recently telling TASS that “Lately, the discourse from Washington has changed and India is no longer being asked to stop buying oil from Russia. In a recent visit to India, the US Treasury Secretary actually said that India can buy discounted oil from Russia as much as it wants so long as western tankers and insurance companies are not used.”

African leaders travel to Moscow. Representatives of 40 African nations traveled to Russia for the Second International Parliamentary Conference “Russia – Africa in a Multipolar World.” According to the press release, the attendees:

… discussed the potential for collaboration across a range of sectors, their contribution to the African continent’s economy and security, and their work in the realms of science and education, politics, and techno-military area.

During the conference, the African continent was invited to work together to form a new multipolar world order. This is especially important given the significant human resources of Africa, which is home to more than 1.5 billion people and has enormous mineral reserves in its soil.

Brazil and Argentina announce a common currency. In February, the two dominant Latin American economies announced plans for a common currency called the “sur” for use in bilateral trade. South America is a big, resource-rich place with numerous grudges against its intrusive northern neighbor. So a de-dollarization movement there, while not as immediately consequential as what’s happening in the Middle East or Asia, is both plausible and potentially serious for the dollar.

First CNN does a segment on de-dollarization, now Fox News also.

What is going on here?

🔊

— Wall Street Silver (@WallStreetSilv) March 27, 2023

Read the full article at John Rubino.

Comment on this article at HealthImpactNews.com.

This article was written by Human Superior Intelligence (HSI)

See Also:

Understand the Times We are Currently Living Through

FREE eBook! The Concept of the American Christian Family is a Myth and is NOT Found Anywhere in the Bible – by Brian Shilhavy

FREE eBook! Restoring the Foundation of New Testament Faith in Jesus Christ – by Brian Shilhavy

The Brotherhood of Satan vs. The Brotherhood of Jesus Christ

KABBALAH: The Anti-Christ Religion of Satan that Controls the World Today

Exposing the Christian Zionism Cult

The Bewitching of America with the Evil Eye and the Mark of the Beast

Jesus Christ’s Opposition to the Jewish State: Lessons for Today

Identifying the Luciferian Globalists Implementing the New World Order – Who are the “Jews”?

The Brain Myth: Your Intellect and Thoughts Originate in Your Heart, Not Your Brain

What is the Condition of Your Heart? The Superiority of the Human Heart over the Human Brain

The Seal and Mark of God is Far More Important than the “Mark of the Beast” – Are You Prepared for What’s Coming?

The Satanic Roots to Modern Medicine – The Image of the Beast?

Medicine: Idolatry in the Twenty First Century – 10-Year-Old Article More Relevant Today than the Day it was Written

Having problems receiving our emails? See:

How to Beat Internet Censorship and Create Your Own Newsfeed

We Are Now on Telegram. Video channels at Bitchute, and Odysee.

If our website is seized and shut down, find us on Telegram, as well as Bitchute and Odysee for further instructions about where to find us.

If you use the TOR Onion browser, here are the links and corresponding URLs to use in the TOR browser to find us on the Dark Web: Health Impact News, Vaccine Impact, Medical Kidnap, Created4Health, CoconutOil.com.