Comments by Brian Shilhavy

Editor, Health Impact News

It appears that the Biden Administration is abandoning their rhetoric that “the banking system is fine.”

CNN reported today that Treasury Secretary Janet Yellen met with CEOs of large banks yesterday and told them that “more bank mergers may be necessary.”

New York (CNN) — During Thursday’s meeting with the CEOs of large banks, Treasury Secretary Janet Yellen told executives that more bank mergers may be necessary as the industry continues to navigate through a crisis, two people familiar with the matter told CNN.

The comments from Yellen provide further evidence that Biden officials are starting to warm up to the idea of bank mergers despite concerns from progressives and the administration’s own scrutiny of corporate concentration. (Source.)

Her statements killed a stock rally this week that saw the stocks of regional banks increase 10%, in one of their best weeks since 2020.

Not anymore.

As ZeroHedge News reported today, reports show that $billions of losses in deposits at U.S. banks have occurred in the past two weeks, with over $70 billion lost in large US Commercial Banks.

After yesterday’s continuing surge on flows INTO money market funds and increase in the use of The Fed’s bank bailout facilities, expectations were for more deposit outflows from US commercial banks (despite Western Alliance’s comments which sparked a melt-up in regional bank shares this week.

However, Treasury Secretary Yellen spoiled the party somewhat today by warning (reportedly) that the market should expect ‘more bank mergers’ (i.e. failures)…

And so, according to the latest H8 report from The Fed, on a seasonally-adjusted basis, total US Commercial Bank deposits fell by $26.4 billion during the week ended 5/10 – the third straight week…

Source: Bloomberg

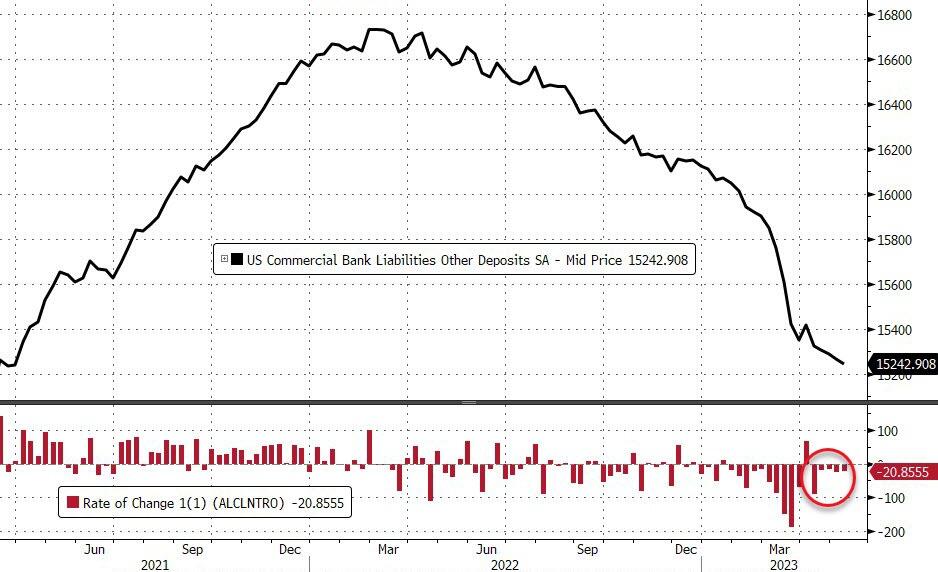

On a seasonally adjusted basis, US commercial bank deposits (ex-large time deposits) decreased $20.8bn last week (during the week-ending 5/10), for the fifth straight weekly outflow. That is the lowest since March 2021…

Source: Bloomberg

On a non-seasonally-adjusted basis, US commercial bank deposits (ex-large time deposits) dropped $50.26 billion (after jumping $63.8 billion) the prior week.

And judging by yesterday’s money market inflows, the deposit outflows continued this week (remember, deposit data is lagged a week to money market and Fed balance sheet data), despite reassurances from WAL…

Source: Bloomberg

On a seasonally-adjusted basis (ex large time deposits), Large, Small, and Foreign banks all saw outflows last week. Small bank deposits are at their lowest since May 2021…

Source: Bloomberg

This is the 5th straight week of Small Bank outflows and Small Banks saw the largest outflows…

- Large Banks -$7.49 billion SA (-$36.5 billion NSA)

- Small Banks -$8.742 billion SA (-$12.5 billion NSA)

- Foreign Banks -$4.627 billion SA (-$1.2 billion NSA)

Source: Bloomberg

Including large time deposits, the breakdown is as follows:

- Large banks -$21.6BN

- Small banks -$2.7BN

- Foreign Banks -$2.1BN

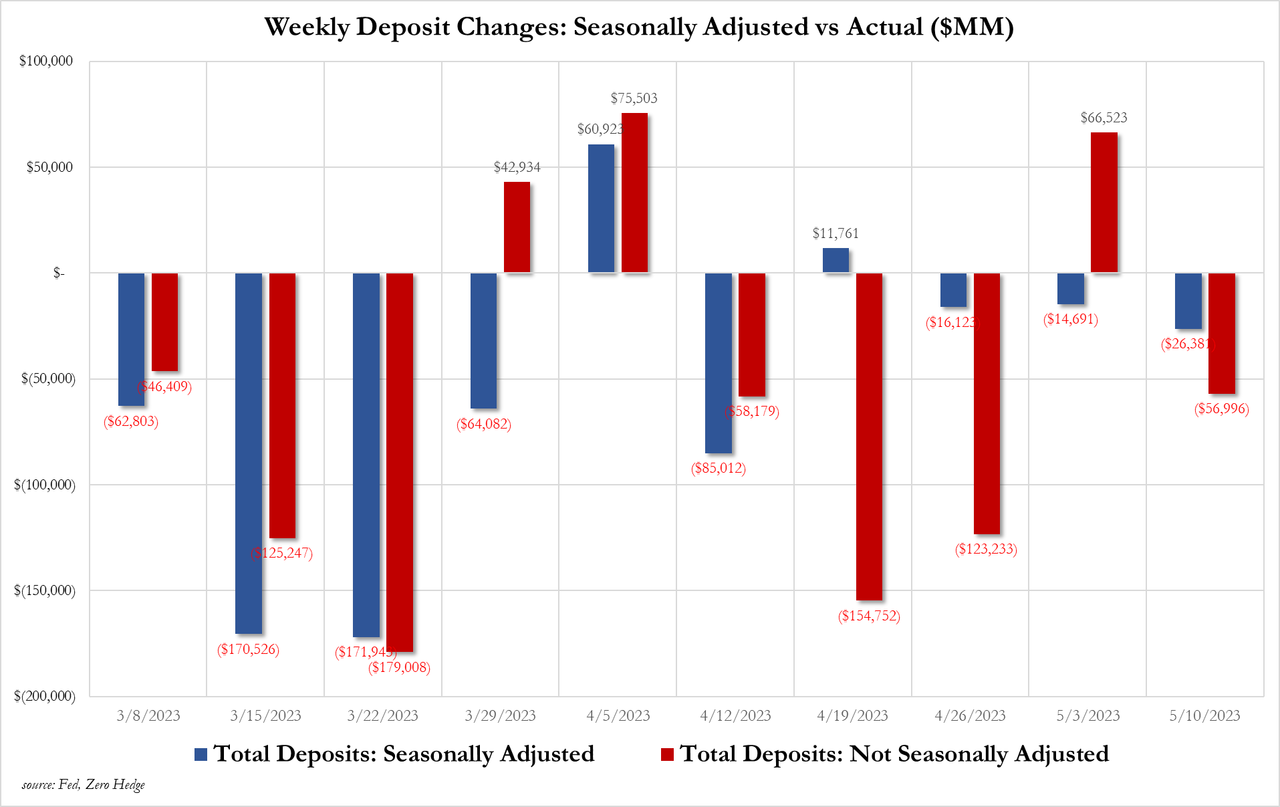

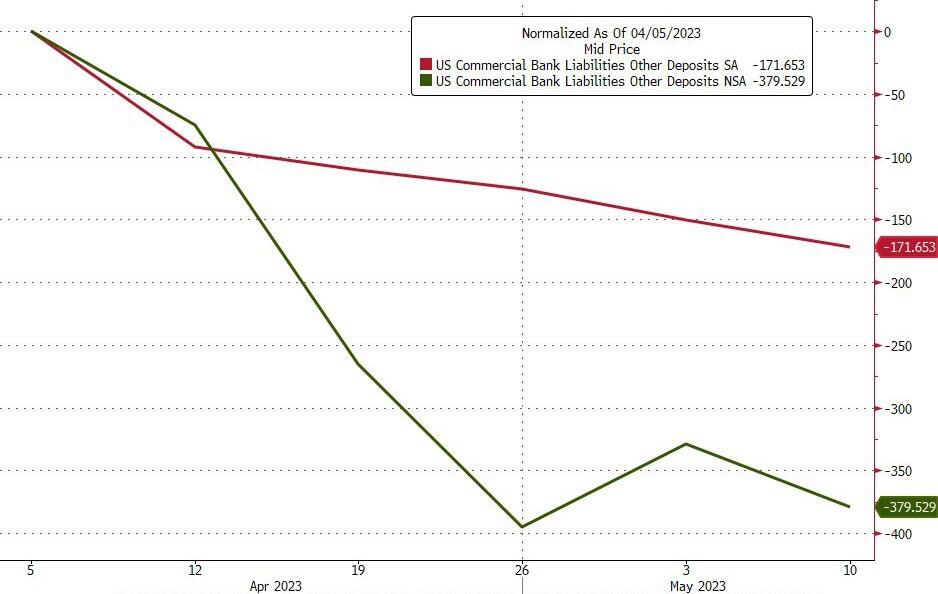

Finally, after adjusting for all the revisions (which are now an every week occurrence), what sticks out to us is that the last 5 weeks have seen $379 billion in NSA bank outflows, while SA the number is an outflow of only $171 billion.

Source: Bloomberg

So The Fed is claiming there are still over $200 billion in tax-payment related deposits expected to return to banks.

Source: Bloomberg

The Fed’s report showed residential real estate loans declined a seasonally adjusted $2.6 billion, while lending for commercial properties rose slightly. Consumer loans also ticked up from the prior week, while commercial and industrial loans fell $3.5 billion.

On the other side of the ledger, Commercial bank lending was little changed in the week ended May 10th, according to seasonally adjusted data. Large bank loans dropped $6.159 billion while Small Bank loans actually rose by $6.85 billion (despite significant deposit outflows)…

Source: Bloomberg

As I wrote yesterday, the entire stock market is now being held up by a few Big Tech companies, and each day I am reading new reports about just how disastrous this could be, because Big Tech is mostly just moving money around right now and trying to buy in on the AI fad.

For example, think about the $10 billion deal that Microsoft paid to OpenAI to start using ChatGPT. $10 billion went on to the books of OpenAI as a gain, but on Microsoft’s books it was entered as a loss.

For the U.S. economy, that is a net zero until Microsoft starts turning a profit and gaining revenue for what they paid to use ChatGPT and started giving it away for free to the public.

Microsoft has huge cash reserves, so they could afford to do something like this, and by giving it away for free, they put pressure on their competitors, especially Google, to hurry up and get their own AI chat software launched.

How long will it take for Microsoft to start seeing a profit with revenue coming in which would benefit the overall U.S. economy?

This is what Goldman’s Sales and Trading desk is saying regarding how long it will take to start seeing benefits from investments in chat AI:

While we are big AI and Chat-GPT enthusiasts ourselves, we tend to be skeptic of significant productivity gains on short time horizons of any new technology.

Even if the new technology can benefit from an existing delivery infrastructure and educated recipients, it should take at least a decade to start having a meaningful impact on a large economy.

On long horizons, productivity boosts from a new technology are temporary as high wages in the most productive sector, in the presence of redistributive taxation, are pushing wages in less productive sectors higher and the most productive sector shrinks in relative employment size and also in relative size to the economy (this is known as the Baumol effect – see Hartwig, Jochen (2001) – “On Misinterpreting the ‘Baumol Disease.'”).

As less productive sectors gain employment the average productivity declines to possibly even lower level. (Source.)

These are actually pretty basic economic principles, but when you look at what investors are doing right now, one has to wonder if this frenzy that is leading to what appears to be uninformed and emotional (primarily fear) economic decisions, is not part of a larger plan, to intentionally cause an economic collapse for the goal of consolidation, in both the banking and Tech sectors.

Related:

Expectations of an Imminent Big Tech Crash Bringing Down the U.S. Economy is Expanding

Comment on this article at HealthImpactNews.com.

This article was written by Human Superior Intelligence (HSI)

See Also:

Understand the Times We are Currently Living Through

FREE eBook! The Concept of the American Christian Family is a Myth and is NOT Found Anywhere in the Bible – by Brian Shilhavy

FREE eBook! Restoring the Foundation of New Testament Faith in Jesus Christ – by Brian Shilhavy

The Brotherhood of Satan vs. The Brotherhood of Jesus Christ

KABBALAH: The Anti-Christ Religion of Satan that Controls the World Today

Exposing the Christian Zionism Cult

The Bewitching of America with the Evil Eye and the Mark of the Beast

Jesus Christ’s Opposition to the Jewish State: Lessons for Today

Identifying the Luciferian Globalists Implementing the New World Order – Who are the “Jews”?

The Brain Myth: Your Intellect and Thoughts Originate in Your Heart, Not Your Brain

What is the Condition of Your Heart? The Superiority of the Human Heart over the Human Brain

The Seal and Mark of God is Far More Important than the “Mark of the Beast” – Are You Prepared for What’s Coming?

The Satanic Roots to Modern Medicine – The Image of the Beast?

Medicine: Idolatry in the Twenty First Century – 10-Year-Old Article More Relevant Today than the Day it was Written

Having problems receiving our emails? See:

How to Beat Internet Censorship and Create Your Own Newsfeed

We Are Now on Telegram. Video channels at Bitchute, and Odysee.

If our website is seized and shut down, find us on Telegram, as well as Bitchute and Odysee for further instructions about where to find us.

If you use the TOR Onion browser, here are the links and corresponding URLs to use in the TOR browser to find us on the Dark Web: Health Impact News, Vaccine Impact, Medical Kidnap, Created4Health, CoconutOil.com.